To see the article on Barron’s website, click here

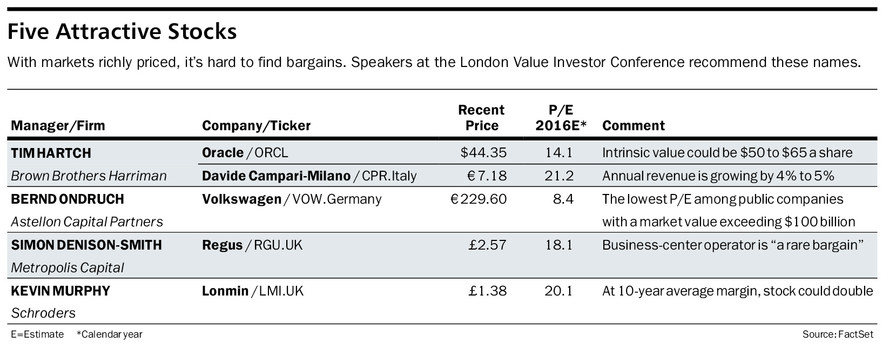

Volkswagen, Oracle, and Davide Campari-Milano, the Italian spirits company, were among the top investment picks of the A-list professionals speaking at last week’s London Value Investor Conference. There was plenty of talk at the charity event—which raised almost $50,000 for Child Bereavement U.K.—of two legendary American value investors, Benjamin Graham, who died in 1976, and his disciple Warren Buffett.

Speakers at this year’s London Value Investor Conference included (clockwise, from top left) Tim Hartch, Simon Denison-Smith, Charles Brandes, Bernd Ondruch, Cheah Cheng Hye, and Kevin Murphy. Photographs: Anna Michell

Charles Brandes, chairman of Brandes Investment Partners, took a potshot at index investing, arguing that it doesn’t contribute to value creation. “It’s a big problem for economic growth,” he said.

Bernd Ondruch, founder of Astellon Capital Partners, praised prospects of German auto maker Volkswagen (ticker: VOW.Germany), whose brands also include Audi, Porsche, and truck maker Scania. The departure in April of Volkswagen’s chairman, Ferdinand Piech, was a positive shift in governance, said Ondruch, noting that the company, still 51%-owned by Piech’s family, had been run more like a family trust for the past 20 years.

Volkswagen could benefit from a shift toward modular technology, Ondruch said. With 335 different models among its brands, the company could cut costs by making several models from the same platform. He sees scope for modularity in 30% of Volkswagen’s line in 2016, which could drive operating profit margins to 8.5% from 6.3% last year.

Vehicle sales in Europe increased last year for the first time since 2007, and the trend could continue in 2015. Volkswagen, with 26% of the market, is a major beneficiary. VW also could shift gears with an initial public offering of its truck business, something Ondruch “fully expects” to happen in the next two years.

VW’s truck division is well placed in emerging markets and has tremendous growth potential in China, where international brands account for only 1% of the market.

Volkswagen trades for 230 euros, or 8.4 times projected 2016 earnings of €27.22 ($30.23) a share. The stock is cheap, argued Ondruch, who once spent three months working at a VW plant after losing his student financing in the stock market. VW has the lowest price/earnings ratio of all publicly traded companies worldwide that have a market capitalization above $100 billion.

Even with a holding-company discount and pension liabilities, VW’s sum-of-the-parts value could reach €165 billion in three to four years, Ondruch said. That represents upside of 60% from the recent price. It is easy to see VW closing the valuation gap with German rivals Bayerische Motoren Werke (BMW.Germany) and Daimler (DAI.Germany), which trade for more than 10 times estimated earnings.

PLATINUM MINER LONMIN (LMI.UK) is another pick that could benefit from the rebound in demand for new cars. Platinum’s main uses are in jewelry and catalytic converters for autos.

Lonmin traded for five times book value in 2007, when it enjoyed fat profit margins. But the company spent heavily to boost production just before the global financial crisis hit and demand dried up. After three rights issues in as many years, the balance sheet has “enough liquidity,” said Kevin Murphy, co-head of the global value team at Schroders.

Lonmin still faces challenges, including excess supply, poor labor relations, and a difficult political backdrop in South Africa. But, at 0.4 times book, it is one of the cheapest stocks in the U.K. Investors could double their money with earnings at 10-year average margins, said Murphy, who expects margins to exceed average levels.

Oracle (ORCL) and Campari (CPR.Italy) were selected by Tim Hartch, who co-manages Brown Brothers Harriman’s Global Core Select fund. Software maker Oracle has a “great track record of creating value,” he said.

Hartch likes the company’s leadership position in database software; its enterprise applications; a loyal base of 400,000 customers; and a growing support business.

Oracle has $20 billion in recurring revenue—more than half its fiscal 2014 revenue of $38.3 billion—and strong profit margins that produced about $14 billion in free cash flow last year. It also has about $10 billion in net cash.

The shares recently traded for $44, or 14.6 times forecast 2016 earnings of $3.02 a share. Hartch puts intrinsic value at $50 to $65 a share, suggesting significant upside.

Campari, whose brands include its namesake spirit, the aperitif Cinzano, and Wild Turkey bourbon, could rally between 10% and 20%. Shares recently traded above €7 a share, or 21 times 2016 projected earnings of €0.34 a share.

Return on capital has dipped due to recent acquisitions, but Hartch thinks increased spending is in the past. Revenue, €1.56 billion in 2014, is growing by 4% to 5% annually.

“The downside is quite limited,” he said.

Hartch recommended Zoetis (ZTS) and Svenska Handelsbanken (SHB-A.Sweden) at last year’s value conference. Shares have gained 57% and 15%, respectively, in the past 12 months.

SIMON DENISON-SMITH, co-founder of Metropolis Capital, likes Regus (RGU.UK), which provides office space in 2,300 business centers worldwide. The company’s investment in expansion masks its true value, he said. Regus trades at 18 times next year’s estimated earnings. Strip out new office space that isn’t yet contributing to cash flow, and the multiple falls to 10.

Regus’ earnings are growing by 20% a year. Even with just 10% growth, Smith thinks the shares are worth £4.70 ($7.28), versus a recent price of £2.57. “Regus is a rare bargain in what has been a challenging market,” he said.

Cheah Cheng Hye cited the potential of Chinese stocks, particularly the H-shares listed in Hong Kong, which have missed the rally in Shanghai. “In many cases, these are the same shares with the same dividends and the same rights,” said Cheah, chairman and co-chief investment officer of asset manager Value Partners Group (806.Hong Kong).

The Hang Seng China Enterprises index trades for around 10 times this year’s projected earnings, compared with a multiple of more than 18 for the Shanghai Composite.

In a question-and-answer session, Brandes said his firm is investing in Russian equities listed in New York (he declined to name them). He thinks U.S. banks are undervalued, but it could be three to five years before they “normalize,” and even then, returns will lag behind those in the past.